Hiding From Tariffs Using ADRs Elsewhere

The Brief: Build a Fortress. Or Failing That, a Reasonable Bunker

The assignment was simple, if bleak: find four emerging-market ADRs (excluding China and Taiwan) that won’t keel over the next time a trade war gets announced in a press conference or a tweet. We can’t do China because tariffs and political risk (which here means asset seizures); we can’t do Taiwan because invasion risk.

The selections should be large enough to survive a storm, local enough not to be caught in one, and dull enough to go under the radar. In other words: companies that can operate profitably while pretending the global trading system isn’t quietly dissolving around them.

The Problem: Globalization Is Still Dressed Up, But the Party’s Over

For all the talk of decoupling, the global economy remains hideously and awkwardly entangled like a pair of dead rattlesnakes caught in flagrante delicto. Supply chains stretch across continents. Trade volumes remain high, for now (thought you wouldn’t know it from the share prices of ship leasing firms). But under the surface, plenty is rotten and there’s no disinfectant without the bust-up WTO. Tariffs, export controls, sanctions, subsidies, bans on chips, bans on minerals, bans on software, bans on platforms that run software that make chips, bans on bans in retaliation to previous bans. It’s whack-a-mole (that word again) geopolitics and it’s only accelerating.

And it’s not just China. Countries across Southeast Asia have been slapped with “precautionary” tariffs under the all-purpose heading of national security. India though, once a peripheral player in global trade, now finds itself courted by every Western power looking for a non-Chinese factory floor. That’s not necessarily good news. Invitations to proxy status come with strings attached.

But Trump is popular in India. That shouldn’t matter, but now we’re doing Theory of Mind for narcissists. Also it’s a long way away geographically and conceptually from DC. Also India has nigh on 1.5 billion people. Can they get thrown around by a tariff tantrum? Yes, but less so, one hopes. This hints at the the key point here. No single individual should be able to tank your portfolio 15% in three days, whether he’s wearing a red tie or not.

So you build a bunker portfolio. Not a collection of plucky exporters or clever strategic plays, but large, inward-facing, domestically-rooted businesses abroad that are, for now, mostly ignored by trade policymakers.

What We’re Looking For

The rules of this game were:

No China. No Taiwan. That’s not cowardice, that’s self-preservation.

Mid or large cap. We’re not hiding in shadows with small caps; we’re hiding behind elephants.

Low tariff sensitivity. No one wants to wake up and find their top line priced out of the market by a new import duty.

Sector and regional spread. Diversify the escape routes.

What emerged was a collection of four EM stocks that barely know there’s a war on. Two Indian behemoths, a Brazilian brewer, and an Indonesian telecom. None of them exciting. All of them plausible survivors.

The Portfolio

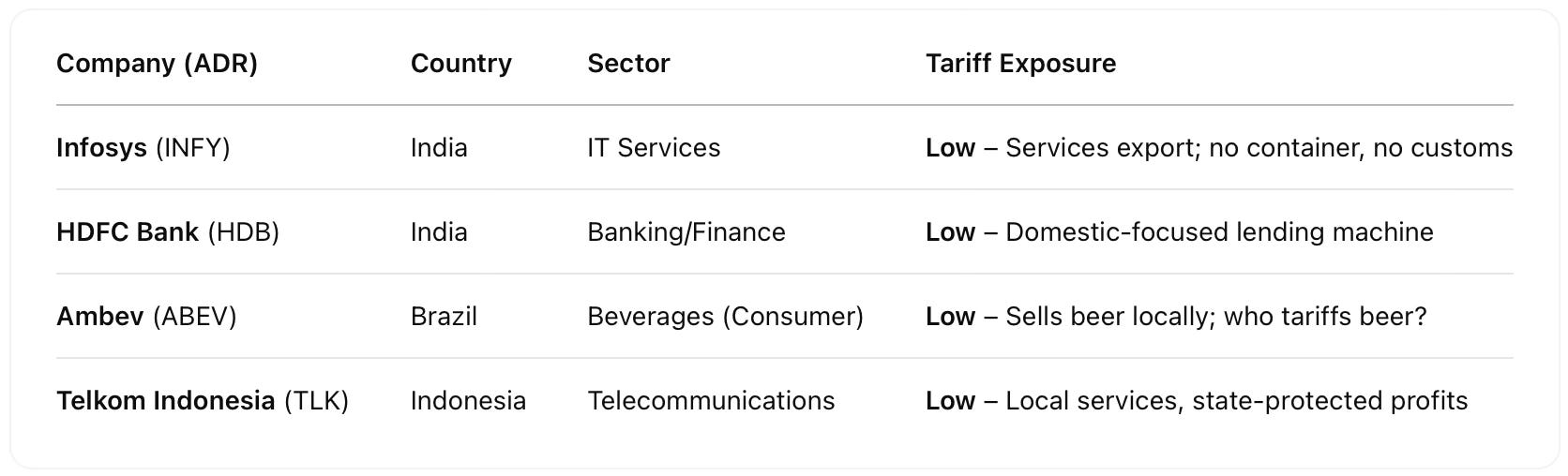

1. Infosys (INFY) – India's Code Factory

India’s most exportable product isn’t textiles or pharmaceuticals -- it’s middle-class competence delivered over fiber optic cables. Infosys sells software services to American and European companies. Its margin structure is envied, its bureaucracy is legendary, and its ability to extract predictable profits from vague deliverables is practically an art form.

Tariffs? Not really a problem. You can’t tax someone for writing code in Bangalore. If clients in the U.S. start cutting spending, maybe that hits the pipeline. But there are no containers to block, no ports to choke, no customs stamps to cancel. Infosys exists in the part of globalization that hasn’t yet been politicized -- and probably won’t be, because no one wants to admit they outsourced their IT department in 2006 and forgot to build a new one.

It’s a $70 billion giant that thrives on other people’s operational gaps. In a world built on inefficiencies, that’s a growth industry.

Note the amazing fact that we’re all talking about tariffs on goods/merchandise when 90% of the US economy is services (as it is in most developed countries). So you have to buy services companies a long way away. Here’s one.

2. HDFC Bank (HDB) – Banking, But Not the Fun Kind

HDFC Bank is India’s largest private-sector bank. It doesn’t fund space startups or buy now/pay never apps. It takes deposits, issues loans, and collects fees. It is, in short, what banks were before fintech got involved. Do not ask me about paperwork in India or how hard it is to deal with legacy banks. Yes they can get taken out by a fintech. But when and how long will it take for the fintechs to get approved?

Most of HDFC’s business is domestic. Mortgages, car loans, credit cards, the kind of stuff people in India still need whether or not two superpowers are arguing about semiconductors. It is also almost aggressively boring. Even its merger with its parent housing lender was executed without drama.

If trade wars drag down global markets, HDFC might wobble a little. But India’s growing middle class still needs financing. The secular story -- more people using more financial services -- remains intact. No containers involved, no sanctions threatened. Just slow, steady accumulation of interest. Note that the government is very focused on expanding the middle class.

Bonus -- India has arguably the world’s most advanced digital ID system which coexists with a numerically enormous unbanked sector. See how that works together?

3. Ambev (ABEV) – Brazilian Beer, Global Indifference

The only thing more stable than Ambev’s cash flow is its product lineup. This is the company that sells Brazil its beer. And in case you haven’t checked, no one’s putting tariffs on lagers. Skol, Brahma, Antarctica -- they move from brewer to bar without crossing an ocean.

Ambev is technically part of AB InBev, but it’s mostly left alone to dominate its patch of Latin America. It has scale, distribution, pricing power, and brand loyalty. That’s useful in a world where trade flows might slow and purchasing decisions get made closer to home.

It also has the great advantage of being ignored. Nobody writes white papers about the strategic role of Ambev in the global economy. That’s perfect. It makes money, pays a dividend, and doesn’t show up on anyone’s sanctions list. A luxury in these times.

Bonus point -- beer is supposed to be good in and out of recessions because you’re always either treating depression or celebrating good times. Bonus bonus point -- have you ever been on Copacabana beach and tried to not drink beer?

4. Telkom Indonesia (TLK) – Local Monopolist in a Nation of 270 Million

Telkom Indonesia is boring, profitable, and mostly owned by the state. It provides telecom services to half the country, and it does it without needing to import much or export anything.

Data services are inherently domestic. There’s no reason to tariff them -- and if someone tried, good luck enforcing it. The real risk here isn’t trade war; it’s state interference. But as long as the government prefers to extract cash via dividends rather than meddle in operations, TLK looks solid.

The company is leaning into digital services -- data centers, fintech, etc. -- but at its core, it’s a utility with a growth curve. You don’t need macro tailwinds when your customer base is expanding by demographic inevitability.

The Table

The Takeaway: When in Doubt, Assume It’s DefCon 1

Globalization isn’t dead -- it’s just in denial. Trade still happens, but everyone’s hedging their bets. The same countries calling for open markets are writing new tariff schedules behind the scenes. The markets might pretend otherwise, but portfolio construction has to live in the real world.

So this is the bunker. It’s not exciting. No one’s going to ring a bell when these companies double. (Actually, I might.) But they’re built to survive the current chaos -- and possibly the next ten rounds of it. They don’t rely on fragile alliances or easily weaponized supply chains. They don’t get whiplash every time someone threatens a tariff on lithium or printed circuit boards.

They just operate. In some cases, they do it quietly. In others, they do it bureaucratically. But most importantly, they do it without needing anyone else's permission.

There’s a case for bravery in investing. This is not that case.

This is a nuclear bunker portfolio -- built to duck, survive, and maybe even thrive while the loudest players on the board get nuked by geopolitics.

With this, I’ve reduced my US exposure to about 25%. You need some, in case they ever get sane. But the system isn’t (yet?) stopping the administration from simultaneously tanking $, stocks and bonds. Normally bonds should go up when stocks go down and vice versa. And trouble in general means the $ goes up because safe haven.

All three tanking at the same time means the end of US exceptionality. The end of trust. International investors are going to remember that for a long time, whatever happens next.

Disclaimer -- this is not financial advice. Disclosure -- yes, I bought all these stocks before I told you about them. About 60 seconds ago. You’re welcome.